Lululemon: A Brand at the Crossroads

We are launching primary research to answer the question the market cannot: is Lululemon's U.S. business broken, or fixable?

✦

Calvin McDonald steps down as CEO on January 31. Elliott Management holds a billion-dollar stake and has named a preferred successor. Founder Chip Wilson is running a parallel proxy fight. The stock has lost $42 billion in market value since December 2023 and trades at its lowest earnings multiple in a decade. We are launching primary research to answer the question the market cannot: is the U.S. business broken, or fixable?

Key Insights

- The stock is down 55% from its peak. Lululemon has lost $42 billion in market value since December 2023. At 14x forward earnings, the multiple is at its lowest level in a decade.

- The CEO is leaving in days. Calvin McDonald steps down January 31. Elliott Management holds $1B+ and has named a preferred successor. Founder Chip Wilson is running a parallel proxy fight with three board nominees.

- The U.S. business is in decline. Americas comparable sales fell 5% last quarter—the first sustained negative comp in the company's history as a public company. Traffic, conversion, and promotional intensity are all moving in the wrong direction.

- Consensus has no conviction. 78% of sell-side ratings are Hold. Price targets range from $175 to $303—a $128 spread. Nobody knows if this is cyclical or structural.

- The catalyst window is compressed. Q4 earnings in March, proxy materials in April, annual meeting in June. The market will form a view in the next two quarters—whether or not it's well-informed.

Participation Opportunity

Woozle Research is inviting professional investors to sponsor or co-sponsor this primary research. Participation is collaborative—all funds receive full access to research outputs including interview summaries, transcripts, and the final synthesis report.

- Launch: February 3, 2026

- Delivery: February 10, 2026

- Participation: Limited to 5 Funds

- Catalyst: CEO departure, proxy fight, stock underperformance.

- Research: 50+ retail store channel checks

- Deliverables: raw data, transcripts, synthesis report, analyst access

Sponsor this research

This research will proceed with a minimum of one fund and is limited to a maximum of five.

Email to confirm your interestThe Catalyst

Lululemon enters 2026 facing a convergence of pressures it has not experienced in over a decade.

The company built its position as the defining brand in premium athleisure. For years, that position appeared unassailable. Revenue tripled under Calvin McDonald's leadership. International expansion accelerated. China became the second-largest market. The men's category grew from afterthought to meaningful contributor.

But the U.S. business—still roughly two-thirds of total revenue—has weakened materially. Americas comparable sales declined 5% in the most recent quarter. Traffic has softened. Promotional activity has increased. Full-price sell-through, once a point of pride, has come under pressure.

The leadership transition compresses the timeline. Elliott Management disclosed its stake in December and has been explicit about its preference: Jane Nielsen, former CFO and COO of Ralph Lauren. Chip Wilson holds approximately 8.5% and has nominated three board candidates, demanding the resignation of the chair and lead director. The board faces pressure from two directions with potentially incompatible objectives.

Q4 earnings arrive in early March. Proxy materials are due in April. The annual meeting follows in June. By the time these milestones pass, the market will have formed a view—whether or not that view is well-informed.

Key Intelligence Questions

The research will focus on the commercial dynamics that determine whether Lululemon's U.S. business stabilises or continues to deteriorate. Each question targets a specific input to the investment model.

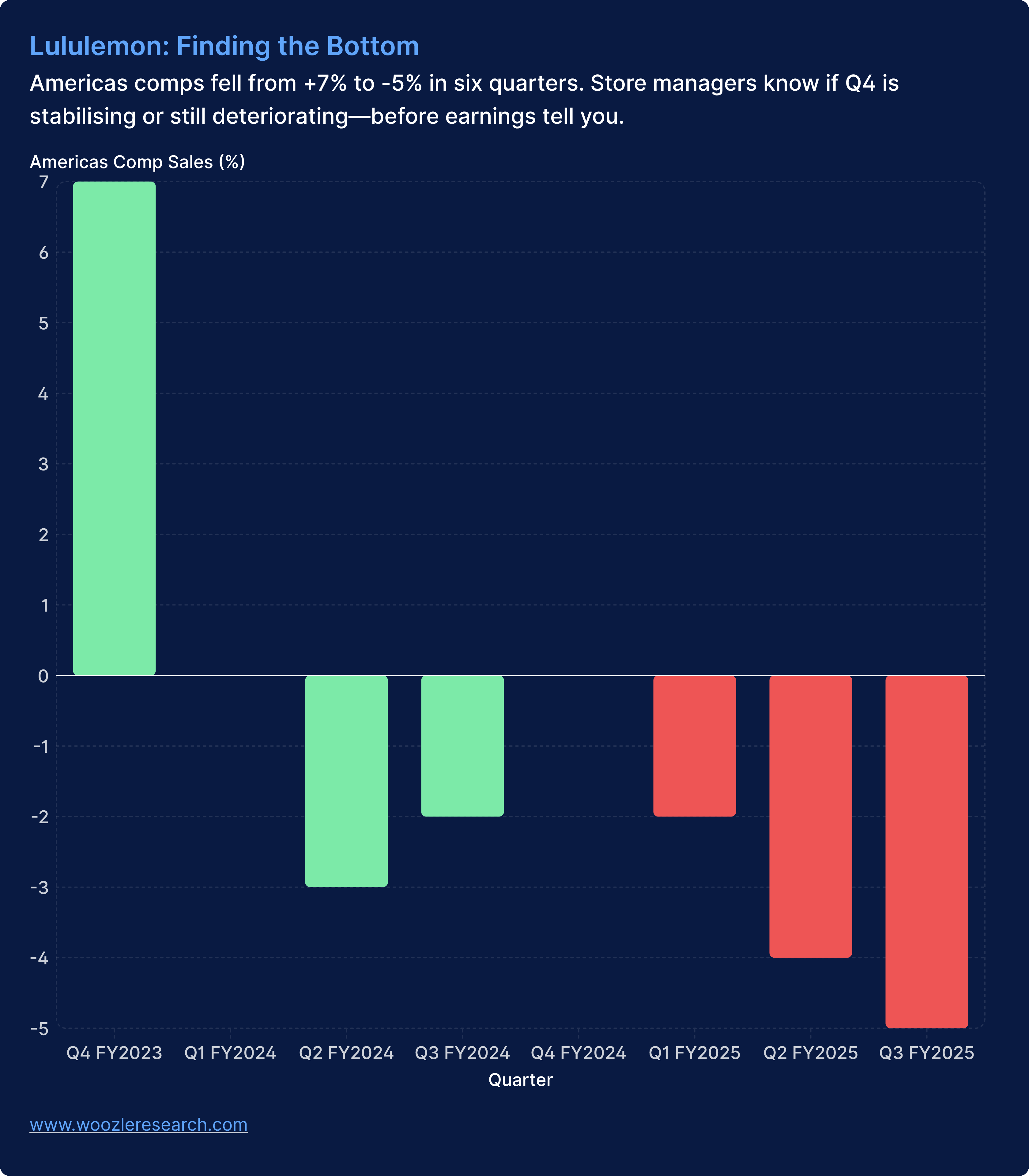

Same-Store Sales: Finding the Bottom

The Q3 Americas comp of -5% is the worst in Lululemon's public company history. Current estimates assume stabilisation in Q4 and a return to flat-to-positive by mid-2026. The bear case says this is early innings.

Sequential trends matter more than the year-over-year headline. A Q4 comp of -3% is a very different signal than -7%. Management doesn't disclose intra-quarter trajectory. Store managers see it week by week.

Key Intelligence Question

- Are weekly trends improving, stable, or deteriorating heading into Q4? Is the business tracking better or worse than Q3 on a sequential basis?

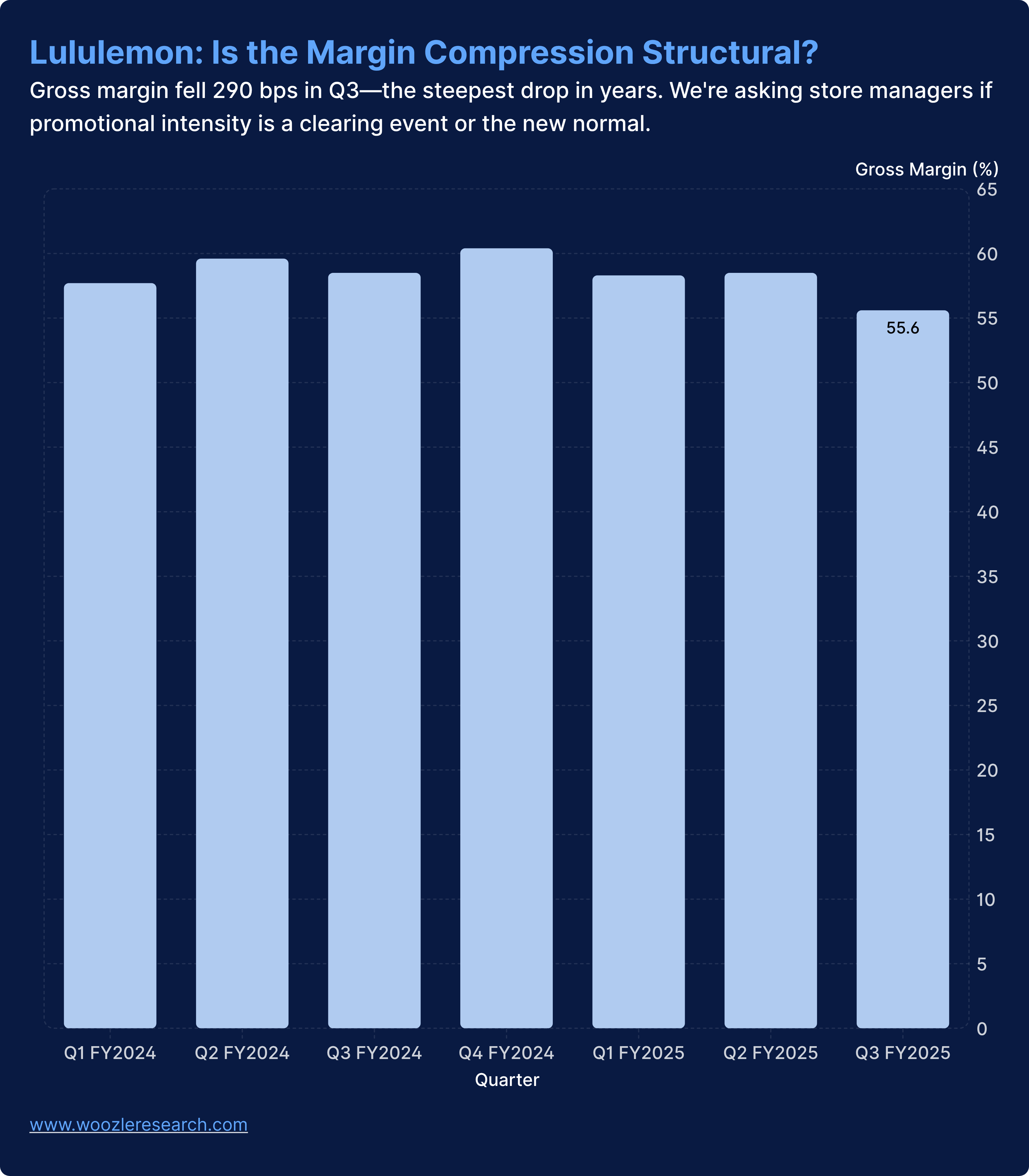

Promotional Depth: Inventory Flush or New Normal?

Gross margin compressed 290 basis points in Q3. Management pointed to promotions and tariffs. The question is whether this is a one-time clearing event or a structural shift in how the brand goes to market.

Lululemon was built on scarcity and full-price selling. If markdown cadence has permanently increased—deeper discounts, broader categories, more frequent events—the margin profile doesn't recover even if comps do.

Key Intelligence Question

- How does current promotional intensity compare to twelve months ago? Is discounting contained to specific categories or spreading across the assortment?

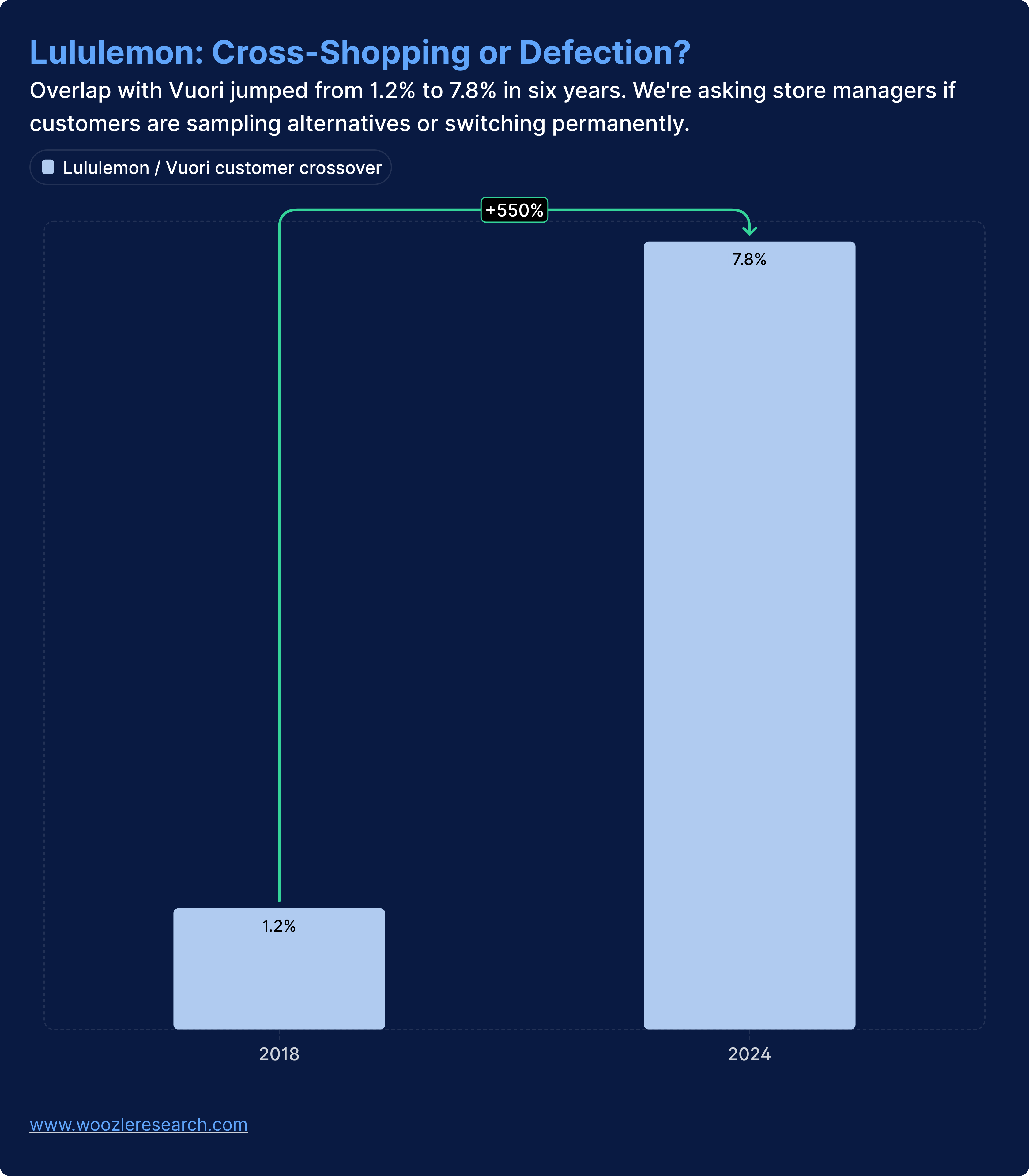

Competitive Displacement: Sampling or Switching?

Customer overlap with Vuori has grown from 1.2% in 2018 to 7.8% today. Alo Yoga is reportedly north of $1 billion in revenue growing 40%. The market knows competition has intensified. It doesn't know whether Lululemon is losing consideration or losing customers.

Cross-shopping is manageable—customers experimenting but returning. Defection is structural—customers who've decided the premium is no longer worth it.

Key Intelligence Question

- When Alo and Vuori come up in customer conversations, is it curiosity or comparison? Are customers trying alternatives and coming back, or switching permanently?

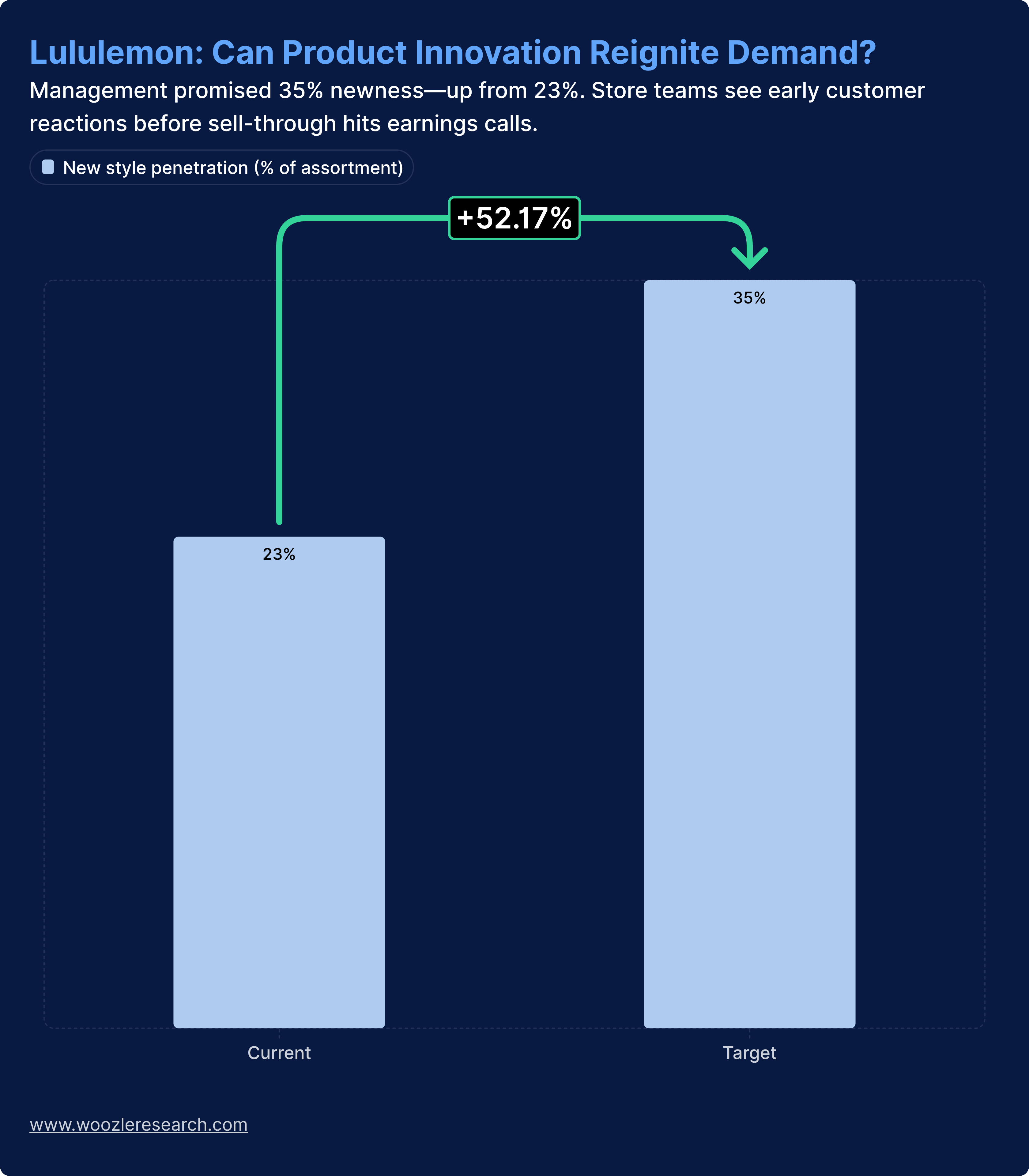

The Spring 2026 Product Bet

Management has acknowledged recent assortments were "too predictable" and promised 35% newness in Spring 2026. The turnaround case depends on product innovation reigniting demand. If the new pipeline underwhelms, the thesis breaks.

Store teams see early customer reactions before sell-through data reaches earnings calls. They know which styles are generating energy and which are sitting. They hear what customers want that doesn't exist.

Key Intelligence Question

- Does the Spring 2026 pipeline read as genuinely differentiated to staff and early customers? Is this a reset or a refresh?

Execution Risk in the Leadership Vacuum

McDonald exits January 31. Interim co-CEOs take over. Elliott wants Nielsen. Wilson wants a board overhaul. Strategic direction is unclear for at least six months—possibly longer if the proxy fight escalates.

Leadership transitions create execution risk before they create strategic risk. Inventory discipline slips. Communication fragments. High performers leave. These signals show up at store level months before they appear in reported numbers.

Key Intelligence Question

- Is there visible execution slippage in inventory management, staffing, or internal communication? How is morale across the store network? Are strong performers staying or exploring options?

How to Participate

Woozle Research is inviting professional investors to sponsor or co-sponsor this primary research. Participation is collaborative—all funds receive full access to research outputs including interview summaries, transcripts, and the final synthesis report.

- Launch: February 3, 2026

- Delivery: February 10, 2026

- Participation: Limited to 5 Funds

- Catalyst: CEO departure, proxy fight, stock underperformance.

- Research: 50+ retail store channel checks

- Deliverables: raw data, transcripts, synthesis report, analyst access

Sponsor this research

This research will proceed with a minimum of one fund and is limited to a maximum of five.

Email to confirm your interestThis document is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Woozle Research conducts primary research on behalf of institutional investors. All research is conducted in compliance with applicable regulations.