Fault Line: Why PE Research Infrastructure Is Breaking

PE holding periods hit 7+ years while add-ons reached 74% of deals. Most research infrastructure is still built for three-year holds. This article breaks down the math on wasted spend, the shifts top firms made, and how to rebuild for the long hold.

✦

Private equity holding periods have nearly doubled in a decade. Add-ons now account for 74% of all deal activity. Some platforms run 10 to 20 acquisitions over a single hold. Yet most firms still operate research infrastructure built for a different era: heavy diligence at entry, a thick report, then gut feel and board decks until exit. That playbook worked when holds averaged three years and value creation came from financial engineering. It breaks when sponsors hold assets for seven years and execute buy-and-build strategies requiring continuous intelligence across dozens of decisions. The math is unforgiving. A platform with 10 add-ons over a seven-year hold, using traditional expert networks with 40% miss rates, wastes $100,000 to $200,000 on research that moves nothing. The firms getting this right rebuilt their infrastructure from the ground up. They stopped buying access and started buying finished intelligence. They moved from episodic projects to continuous operating systems. They tied provider economics to decision impact, not call volume. The rest are burning capital on a model designed for a market that no longer exists.

The numbers that changed everything

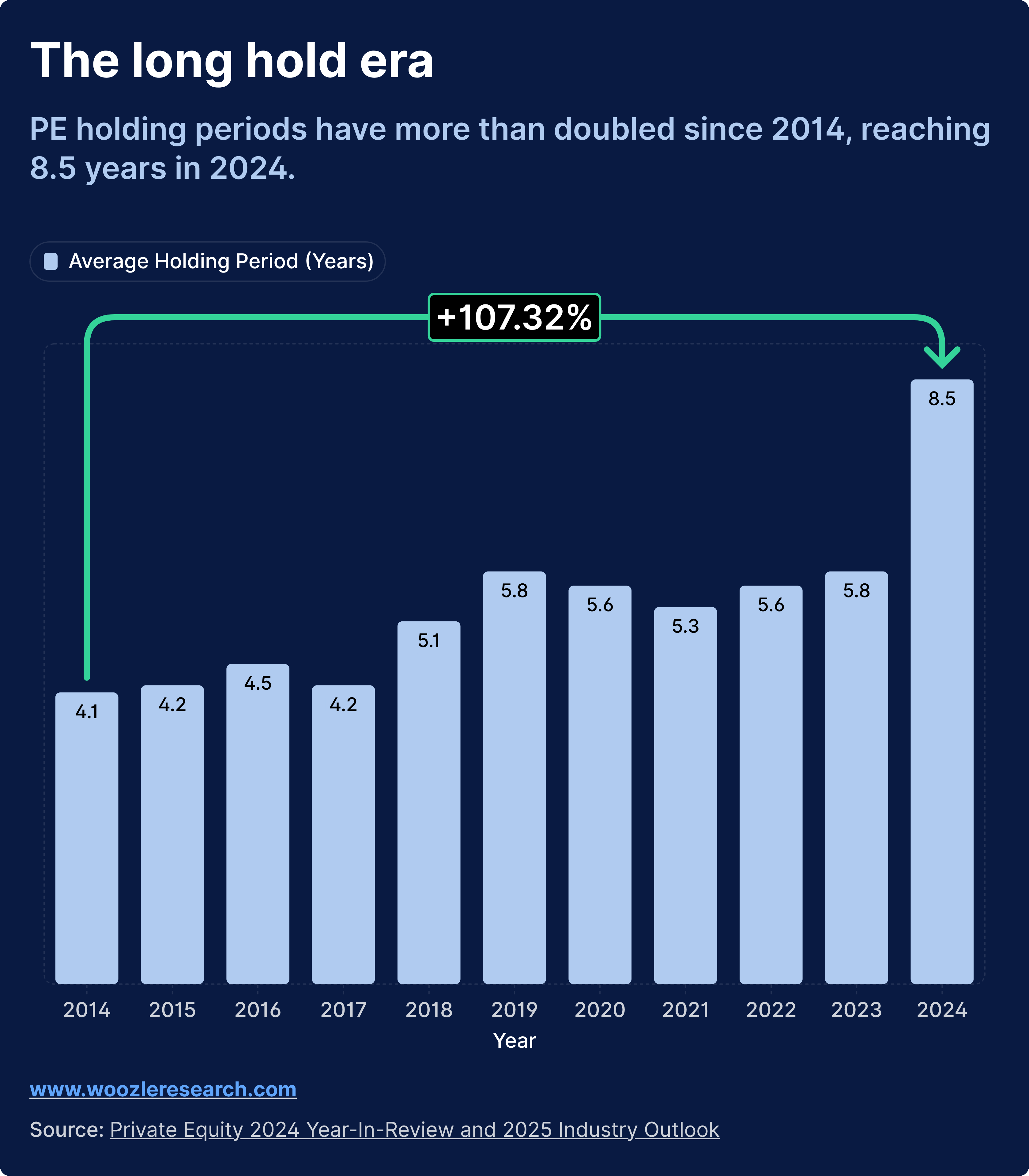

North American PE funds held portfolio companies for an average of 7.1 years in 2023. That figure represents the longest average hold since at least 2000. Globally, the median reached 5.8 years, nearly double the three-year norm from a decade earlier.

Exit markets tightened. Multiple expansion stopped doing the work. Sponsors now hold longer to execute operational plans, prove synergies, and demonstrate real value creation before going to market. The days of buying, levering, and flipping in 36 months are largely over for mainstream PE.

Add-ons account for 74% of all PE deal activity. The buy-and-build thesis dominates. Some platforms execute 10 to 20 bolt-on acquisitions in just a few years, each requiring its own diligence, each presenting integration risk, each demanding fresh research on customer overlap, competitive positioning, and synergy realization.

Commercial diligence is no longer a one-time event at platform acquisition. Firms now run repeated primary research projects throughout the hold. Every add-on needs work. Every value-creation initiative demands fresh intelligence. Pricing reviews, market entry decisions, repositioning strategies, competitive benchmarking. The research burden multiplied. The infrastructure stayed the same.

How the old model worked

The traditional approach was straightforward. Run heavy commercial diligence at entry. Engage an expert network. Conduct 15 to 25 calls. Write a thick report covering market size, competitive dynamics, customer sentiment, and growth runway. Make the investment decision. Then rely on management updates, board decks, and pattern recognition for the next 36 months until exit.

This worked when value creation came mostly from financial engineering and multiple expansion. Buy at 8x, lever it, grow EBITDA modestly, exit at 10x. The diligence report justified the entry. Everything after that was execution and patience.

The model breaks when sponsors hold assets for five to eight years. It breaks when buy-and-build strategies require evaluating four to twenty bolt-ons, each with its own market position, customer base, and integration complexity. It breaks when LPs and secondary buyers demand evidence that value-creation plans actually happened, not just leverage doing the work.

Infrastructure built for three-year holds cannot support seven-year execution. The gap shows up in wasted spend, missed signals, and decisions made on stale information.

"Infrastructure built for three-year holds breaks at seven."

What longer holds actually require

Every add-on needs its own research spine. Customer overlap analysis. Integration risk assessment. Competitive positioning. Real synergy validation, not assumptions about scale benefits. When a platform runs 15 acquisitions over six years, that means 15 separate research projects layered on top of ongoing portfolio monitoring.

Every value-creation initiative demands fresh work. Is the pricing power thesis holding? Are customers actually adopting the new product? Is the sales force execution improving? These questions cannot be answered with the entry report. They require continuous intelligence tied to milestones and board calendars.

The smartest deal teams spotted early warning signs that would have been invisible under the old model. Churn creeping in a key cohort. A competitor taking share in a micro-segment. Customer satisfaction declining after an integration. Pricing power eroding beneath stable headline numbers.

Continuous intelligence makes these patterns visible before they become write-downs. Episodic reports discover them at exit prep, when options have narrowed and leverage has shifted to the buyer.

Research as an operating system

Leading firms moved from one big report at entry to continuous, decision-linked programs that track performance throughout the hold.

Instead of heavy diligence followed by gut feel, they run frequent pulses. Standing surveys that track customer behavior, pricing power, competitive share, and NPS. Expert interviews tied to specific decisions rather than general coverage. Customer cohort analysis that surfaces variation hidden in aggregate numbers.

The cadence matches the portfolio rhythm. Quarterly pulses aligned with board meetings. Deep dives before major capex or M&A decisions. Rapid-turn projects when competitive threats emerge or management narratives need stress-testing.

Research moved from a project to an operating system. The entry report became the baseline, not the endpoint. Everything after that builds on it, updates it, and challenges it with fresh data.

"Research moved from a project to an operating system."

Buy-and-build intelligence infrastructure

Top sponsors treat research as infrastructure for sourcing and underwriting bolt-ons, not just validating platform investments.

Better teams map sub-scale targets by micro-segment, customer mix, and technology stack before bankers pitch. They know which assets fit the thesis and which introduce integration risk. They have intelligence on competitive positioning and customer overlap before the first meeting.

Targeted work on each add-on reveals where synergies actually come from. Not assumptions about procurement leverage or back-office consolidation. Specific findings on customer overlap, cross-sell potential, and operational fit. Findings that get tested against reality after close.

Results roll into a single view of platform positioning and synergy realization. Not disconnected reports sitting in different folders. An integrated picture that shows cumulative progress and surfaces gaps in the value-creation plan.

Top sponsors treat research as infrastructure for buy-and-build execution: mapping targets before bankers pitch, validating synergies before LOI, and tracking realization after close.

De-risking execution throughout the hold

Tougher exits put value-creation plans under scrutiny. LPs and secondary buyers want evidence that operational improvements actually happened. Management presentations claiming transformation need independent validation.

Smart teams benchmark portfolio companies against peers on pricing, product fit, customer satisfaction, and talent quality. Then they re-run those benchmarks during execution to measure progress. The question shifted from "Is this a good buy?" to "Are we closing the gap quarter by quarter?"

They stress-test management narratives with independent customer data before major decisions. Does the product roadmap resonate with actual users? Is the salesforce execution improving or is management cherry-picking wins? Are customers actually seeing the integration benefits that justified the last add-on?

Exit prep starts years before exit. The data that supports the equity story gets built continuously, not assembled in a rush when the market window opens. Buyers see evidence trails, not claims.

"The question shifted from 'Is this a good buy?' to 'Are we closing the gap quarter by quarter?'"

The compounding cost of the old model

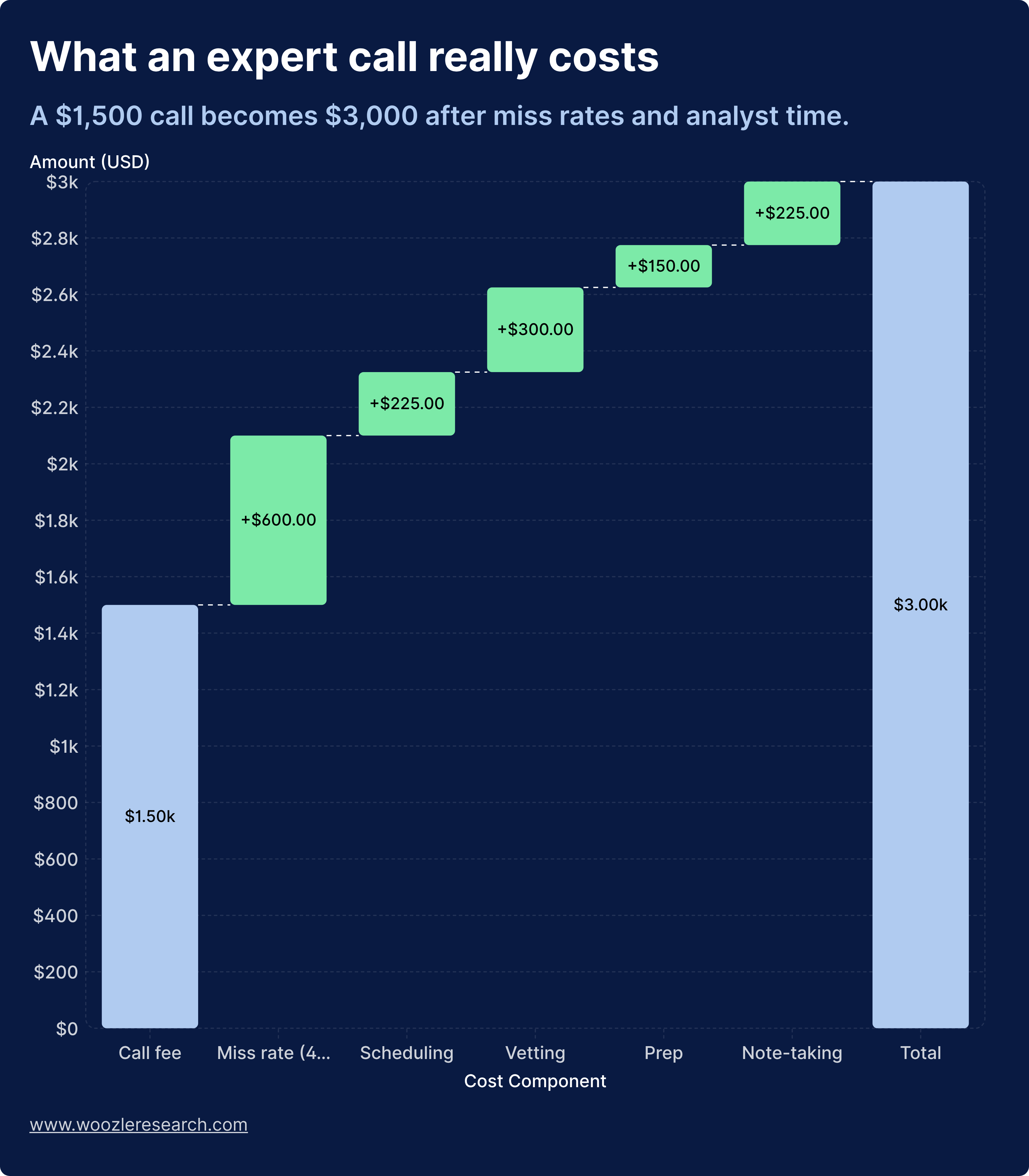

If a platform requires diligence on the initial acquisition plus 10 add-ons over seven years, and each project involves 8 to 12 expert calls at $1,200 with a 40% miss rate, wasted spend alone exceeds $100,000 to $200,000.

That calculation covers only vendor fees. It does not count the 14 or more analyst hours monthly spent on logistics. Vetting expert profiles. Coordinating schedules. Sitting through calls that go nowhere. Taking notes. Chasing transcripts. Summarizing findings for people who were not on the call.

The longer the hold, the more this compounds. A seven-year hold with active buy-and-build execution might involve 50 to 100 expert calls across the platform. At $2,500 to $3,500 per useful insight when analyst time and failure rates are included, the true cost approaches $150,000 to $350,000. Much of it wasted on calls that never touched a model or changed a decision.

The opportunity cost is harder to measure but equally real. Those analyst hours could have gone to deeper modeling, wider watchlist coverage, or better support for portfolio operations. Instead, they disappeared into scheduling emails and note-taking for calls that produced nothing actionable.

The compounding cost of the old model: vendor fees are just the beginning. Analyst time and 40% miss rates push total waste above $100K-$200K per platform over a seven-year hold.

"The cost per platform scales with holding period and add-on count. Most firms never calculate the total."

How to rebuild

Firms getting this right stopped paying for access and started buying finished intelligence. They treat primary research as a continuous operating expense tied to portfolio value, not a one-time project cost buried in deal fees.

Workflows protect analyst time. Ten-minute briefs instead of hour-long intake calls. Zero scheduling burden. No sitting through calls. No note-taking. Outputs arrive ready to drop into models and IC decks, not as raw transcripts requiring hours of synthesis.

Performance-based pricing ties provider incentives to decision impact, not call volume. If the research does not enhance conviction, sizing, or timing on a position, the fee structure reflects that. Providers earn more when their work moves decisions. They earn less when it produces coverage without conviction.

The match matters. Research infrastructure should reflect holding period and strategy. A three-year hold with no add-ons can survive the old model. A seven-year hold with 15 bolt-ons cannot. The firms that recognized this earliest built competitive advantage in deal sourcing, underwriting accuracy, and exit preparation.

Closing thoughts

Holding periods doubled. Add-ons hit 74% of deal activity. The one-report model that worked for three-year holds breaks completely when sponsors execute buy-and-build strategies over seven years.

The math is simple. Platforms need continuous research across the hold. Every add-on requires focused work. Every value-creation initiative demands fresh intelligence. Traditional expert networks with 40% miss rates waste $100,000 to $200,000 per platform in direct costs alone, plus uncounted analyst hours lost to logistics.

Leading teams rebuilt around three shifts. Research as an operating system, not a one-time project. Buy-and-build intelligence infrastructure that maps targets and validates synergies before LOI. Execution tracking that de-risks exits by proving value creation happened.

The new model looks different. Finished intelligence instead of access. Zero-logistics workflows that protect analyst time. Performance-based pricing tied to decision impact. Continuous programs instead of episodic reports.

The question for every PE research function is whether the infrastructure matches the strategy. If the firm holds for seven years and runs 15 add-ons, but the research model still assumes a three-year flip, the gap will show up in wasted spend, missed signals, and exits that underwhelm.

The market changed. The playbook has to change with it.